Compliance means you followed the rules and avoided the penalty. Optimization means you kept the most money legally available to you. Those are two separate calculations, and most business owners only ever get told about the first one. The gap between them is where money quietly leaks out of a business every year.

I'm Marcus Mire, CPA and founder of MireGroup CPAs in Lafayette, Louisiana. After a lot of years of these conversations, here's what I've noticed. The strategies are not secret. The safe harbor rule is published. Cost segregation is written into the code. Nobody is hiding any of this from you.

But knowing the rule and being in position to use it are two different things.

What follows is three examples of that gap. Different topics. Same lesson sitting underneath all of them.

Why do business owners overpay their quarterly estimated taxes?

Because they only run one calculation when there are actually two.

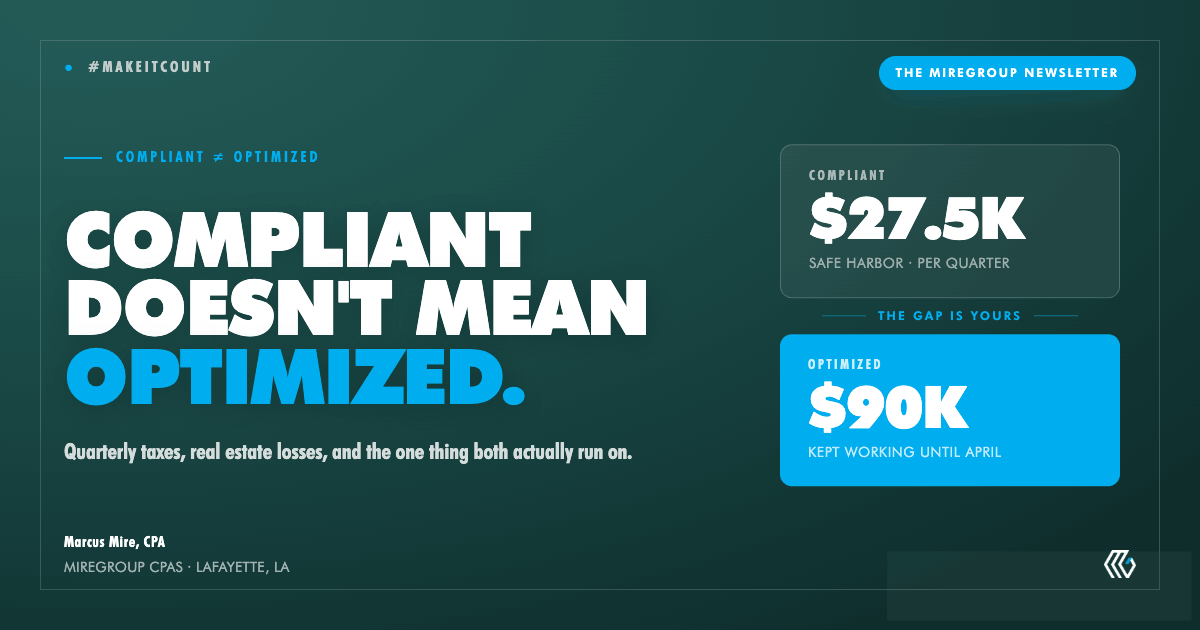

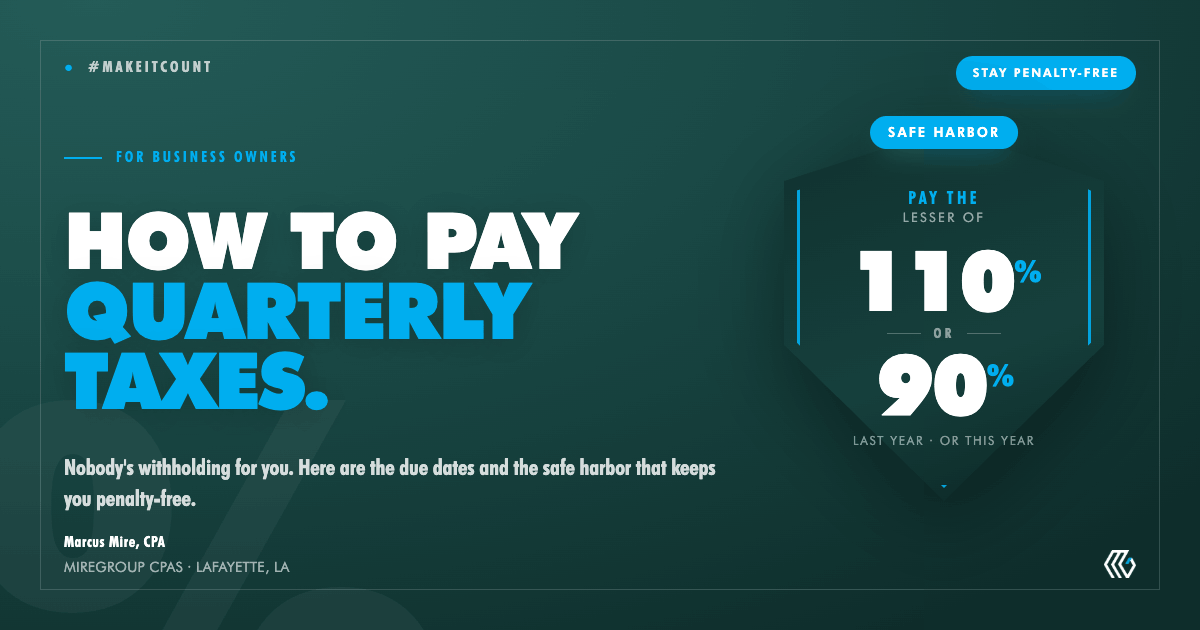

Here's the setup. Last year's tax was $100,000. Your safe harbor is $110,000, which is roughly $27,500 a quarter to stay penalty free. Then you have a big year. You file, and your actual tax comes in at $200,000.

You had two options. Chase the current year and pay in about $45,000 a quarter. Or pay the $27,500 safe harbor, set the remaining $90,000 aside, and pay it when you file in April.

Both avoid the penalty. Both are completely legal. But one of them means $90,000 sat in a high yield account earning for you all year instead of sitting with the IRS.

Look. There are two numbers running at the same time. What you have to pay in to stay penalty free, and what you actually owe. Most people only ever get told about the first one.

You can't run the second one on a guess. It takes a real projection of where the year is landing, and a projection takes current, accurate books. Estimates somebody handed you last spring were a snapshot. Your business is a moving picture.

The principle: compliant and optimized are two different numbers. Somebody has to be calculating both.

Full walkthrough: How to Pay Quarterly Taxes as a Business Owner

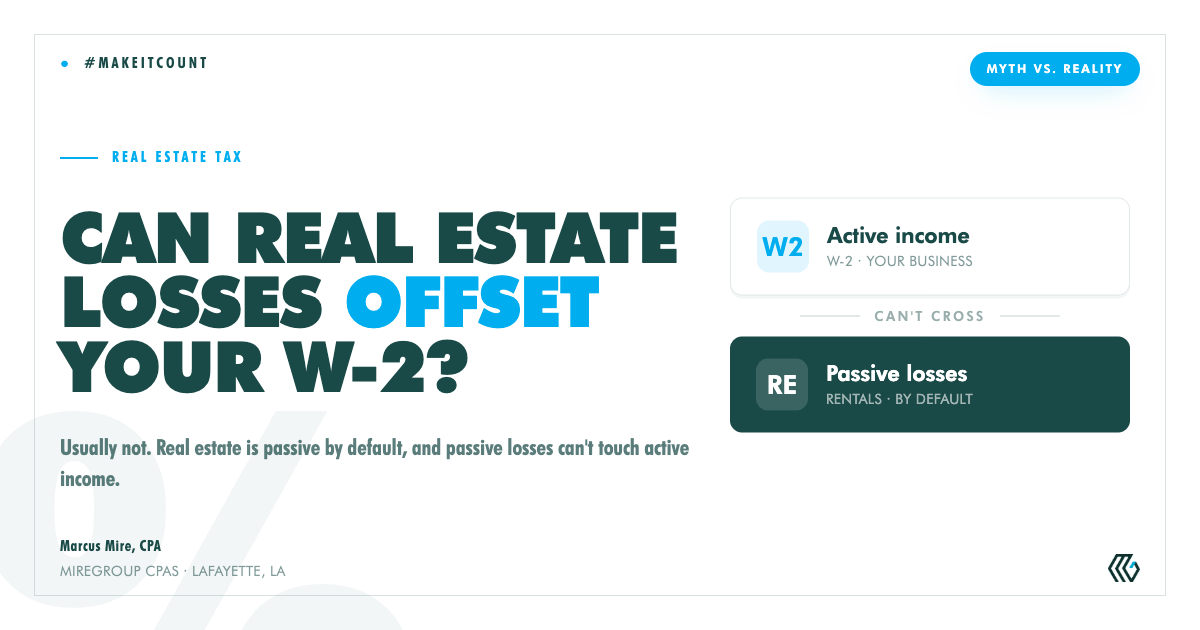

Can real estate losses really erase your W-2 or business income?

Usually not, and the 60 second clip is where that gets lost.

You've seen the videos. Buy a short term rental. Run a cost segregation study. Erase the tax on your W2 or your business income.

The pitch is real right up to a point. You can create the paper loss. That part is true.

Then it stops. Real estate is passive by default in the tax code, and passive losses generally cannot offset active income. So for most people the whole thing falls apart right there.

There are legitimate ways out of the passive bucket. The short term rental route needs an average guest stay of seven days or less, and you still have to materially participate. Miss that second half and you're right back where you started.

What's the tell that a real estate tax strategy is being oversold?

Here's the part that matters even if you never buy a rental in your life.

The firms that do real estate tax work really well will not take you on as a client if you don't have great records. Be cautious of the opposite. A CPA who says they'll take your word for it that you materially participate isn't protecting you. The ones who make you go get a time log before they'll sign off are.

That friction is a feature, not a bug. It's what makes the position defensible if you're ever audited.

Every strategy has a headline and a fine print. The headline is what gets the views. The fine print is what decides whether it works. And the fine print is almost always documentation.

The principle: if someone is pitching it as easy, pause and ask the question.

The full breakdown, including material participation and the real estate professional path: Can Real Estate Losses Offset Your W-2 or Business Income?

Why does July matter more than February for tax planning?

Because both of the strategies above have an expiration date, and February is on the wrong side of it.

Tax preparation is compliance. It's taking last year's data and filing an accurate return. You need it, and you need it done right. But by the time you're sitting across from somebody in February, the year is over. The decisions are made. The money is spent or it isn't. That's the rear-view mirror.

Tax planning is a conversation in July about a decision you're making in October. How you pay yourself, what you buy, when you buy it, which election you make. All of that is still moveable right now. None of it is moveable in April.

Here's a simple test. When was the last time your CPA called you before December 31 to talk about a strategic move?

If the answer is never, you're getting preparation. That's not a knock on them. It's just what the engagement is, regardless of what it says on the invoice. This is why we build advisory meetings into the year instead of waiting for filing season, and it's why the most expensive tax mistakes are almost always timing mistakes.

The principle: preparation keeps you compliant. Planning keeps you ahead. Both matter. Only one changes the outcome.

What do all three of these have in common?

Every one of them runs on the same fuel. Current, accurate numbers, and somebody looking at them before the year closes instead of after.

The safe harbor play needs a projection. The real estate position needs a log. The planning moves need clean books and a calendar that isn't February.

That's the whole thread. Not a loophole. Not a secret. Just being in position to use what's already public.

If any of that sounds like a conversation you'd like to have, we'd love to help.

Get this in your inbox

Make It Count is our newsletter for business owners who'd rather see the move coming than hear about it in April. Real strategies, plain language, no fluff.

Sign up here

Frequently asked questions

Is paying the safe harbor amount instead of my full tax bill legal?

Yes. The safe harbor is a published IRS rule. If you pay in the required percentage of last year's tax through your quarterly estimates, you avoid the underpayment penalty even if you end up owing more at filing. What changes is timing, not the amount you owe. You still pay the full balance in April. The difference is who holds the money in the meantime.

Is there a downside to holding the money instead of paying it in?

The obvious one. If you set the money aside and then spend it, April is going to hurt. This only works if the cash actually stays put and somebody has projected the real number so you know how much to reserve. Discipline is the whole strategy.

Can I use a short term rental to offset my business income?

Possibly, but two conditions have to be met, not one. The average guest stay has to be seven days or less, and you have to materially participate in the activity. Most of the pitches online cover the first condition and skip the second. Missing the second one puts you right back in the passive bucket.

What kind of documentation do I need for a real estate tax position?

A contemporaneous time log at minimum. Not a reconstruction you build the week before an audit. If a CPA is willing to take your word for it on material participation without asking for records, that should worry you rather than reassure you.

When should I start tax planning for this year?

Now, if you haven't. Summer is the stretch where you can still change what happens in April. By December most of the levers are gone, and by February all of them are. The point of planning is that it happens while the decision is still a decision.

Marcus Mire is a CPA and the founder of MireGroup CPAs in Lafayette, Louisiana. MireGroup provides subscription-based accounting, tax planning, and advisory services to small business owners. See how we work or talk to us.