Tax planning should build your wealth. But two of the most common moves small business owners make during tax planning do the opposite. They feel productive. They sound smart. And they cost you money.

At MireGroup, we see these two mistakes more than any others: defaulting to equipment purchases for the write-off, and electing S Corp status without running the analysis. Both come from the same place. Both get recommended by well-meaning professionals. And both represent what we call lazy tax planning.

If you're not sure what we mean by lazy tax planning, start here: Tax Planning vs Tax Prep. Understanding the difference between tax preparation and tax planning is the first step toward making smarter decisions with your money.

Mistake 1: Buying Equipment Just for the Tax Write-Off

"My CPA said I need to go spend money before year-end."

We hear some version of this every year. And every year, we have the same conversation: spending money to save on taxes only makes sense if the purchase makes business sense first.

Here's how accelerated depreciation actually works. Let's say you buy a piece of equipment for $100,000. Under current rules, you can take accelerated depreciation and write off the full $100,000 in the current year. If you're in the highest federal bracket at 37%, plus Louisiana's 3% state rate, that $100,000 deduction saves you about $40,000 in taxes.

Sounds great. But you still paid $100,000 for the equipment. The tax savings covered $40,000 of it. You're still out $60,000.

That's the math most people skip. You're spending a dollar to get forty cents back. If you needed the equipment anyway, the depreciation is a sweetener to the deal. It's the thing that puts you over the line from "I was on the fence" to "this makes sense now." That's the right way to use it.

But buying equipment you don't need, or buying a vehicle in December because someone told you to "go spend money"? That's not tax planning. That's a wealth transfer in the wrong direction.

The principle is simple: every business decision should make economic sense on its own. The tax benefit is the bonus, not the reason. If the purchase doesn't improve your operations, increase your revenue, or create meaningful efficiency, the write-off doesn't change the equation enough to justify it.

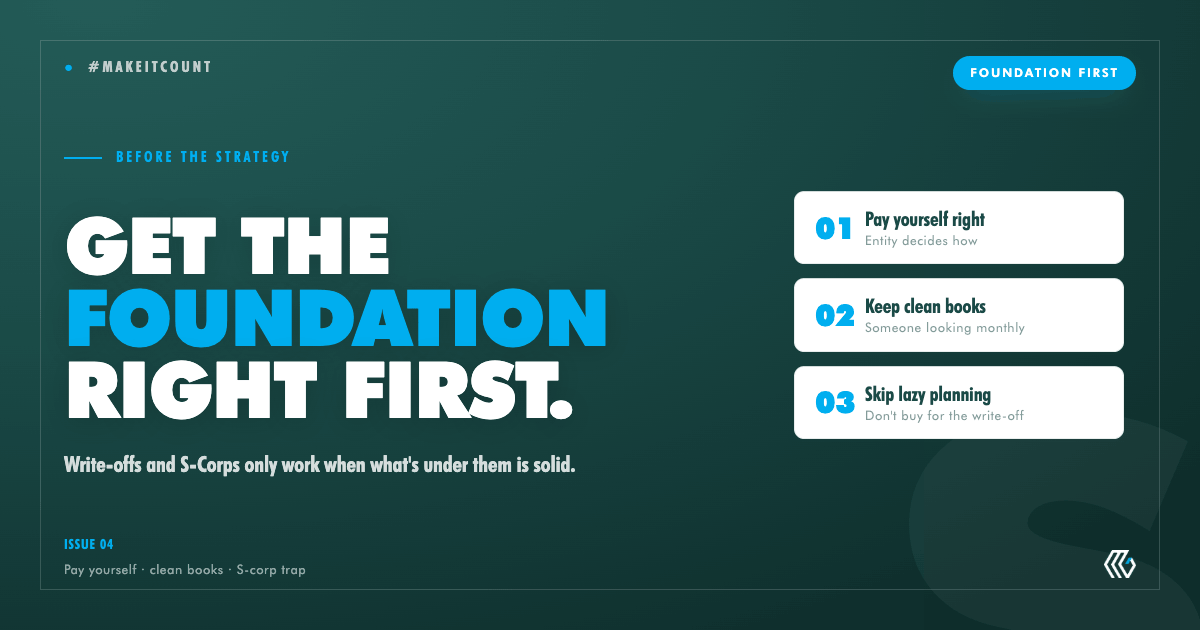

This is exactly the kind of analysis that becomes possible when you have clean, accurate, timely financial data to work from. When your books are right, you can see whether a purchase actually makes sense for your business, not just your tax bill. That's why we believe bookkeeping is the foundation of real tax planning.

Learn more in our full video here:

Mistake 2: Defaulting to S Corp Without Running the Numbers

The second mistake we see is business owners who default to an S Corp election without doing the math on whether it actually benefits them.

Let's be clear: S Corp elections can be a powerful tax planning tool. We've made them for clients when the numbers support it. But we don't default to it. And the difference between defaulting and analyzing matters a lot.

When you're a sole proprietor, you're eligible for the Qualified Business Income (QBI) deduction, which can reduce your taxable income by up to 20%. You don't have to run yourself on payroll. You avoid the administrative costs of an S Corp: payroll processing, additional tax filings, compliance requirements, and the rigidity that comes with corporate structure.

S Corps are significantly more inflexible than a sole proprietorship or partnership. There are rules about shareholder classes, reasonable compensation requirements, and distribution protocols. For some businesses, that structure makes sense and the self-employment tax savings justify the overhead. For others, it doesn't.

The lazy approach is to skip the analysis and just say "you should be an S Corp" because it's the default recommendation in the industry. The strategic approach is to model both scenarios: what does it look like to stay a sole proprietorship with higher QBI and lower administrative costs versus what does it look like as an S Corp with payroll savings but additional overhead?

You need to know the numbers before you make the election. Run the analysis. Compare the total tax picture, not just one line item. If S Corp saves you money after accounting for everything, elect it. If it doesn't, stay where you are.

This kind of entity structure analysis is a core part of what real tax planning looks like. It's the kind of proactive, numbers-driven decision-making that happens when you're working with a CPA throughout the year, not just at filing time.

The Common Thread: Make Economic Sense First

Both of these mistakes come from the same root cause: letting the tax tail wag the business dog.

Equipment purchases should make your business stronger. Entity elections should match your business reality. The tax benefits attached to either decision should be a bonus that makes a good decision even better. They should never be the primary motivation.

When someone tells you to "go spend money" before year-end, ask why. When someone tells you to elect S Corp, ask them to show you the comparison. If the answer is "because it saves on taxes" without any deeper analysis, that's a red flag.

Real tax planning is strategic. It's proactive. And it starts with accurate financial data that lets you model decisions before you make them. That's the kind of work that saves our clients real money, like the client we saved $35,000 through proactive planning last year, or the one who saved $40,000. Neither of those results came from buying a truck in December.

They came from having clean books, a strategic plan, and a CPA who was looking through the windshield instead of the rear-view mirror. That's what proactive tax planning looks like.

Build a Tax Plan That Actually Builds Wealth

If you're tired of year-end scrambles and generic advice, it might be time for a different approach. At MireGroup, our subscription-based model means we're in your books throughout the year, which means when tax planning season comes, we already have the data to make strategic moves.

Explore our accounting and tax plans at mire.group/accounting-and-tax-plans, or reach out to start a conversation.

Marcus Mire is a CPA and founder of MireGroup CPAs in Lafayette, Louisiana, specializing in subscription-based accounting and proactive tax planning for small business owners.