How Do Quarterly Estimated Taxes Work for Business Owners?

If you own a business or do consulting or gig work, nobody is withholding taxes from your income. The IRS runs a pay-as-you-go system, and so do the states. You are expected to pay in as you earn, not all at once in April. That means calculating and paying estimated taxes four times a year, and if you miss the mark, you owe interest on top of the tax.

I'm Marcus Mire, CPA. At MireGroup in Lafayette, Louisiana, this is a conversation we have with clients constantly. Here is how it works, and how to do it well.

Why do business owners have to pay taxes quarterly?

When you have a W2 job, taxes come out of every paycheck. You are not really paying them at that moment. They are being withheld. You settle up when you file your return, and most people get a refund or owe a small amount.

Business owners do not have that safety net. Consulting income, gig work, distributions, none of it comes with withholding. So the job of paying in falls on you. The IRS calls it pay-as-you-go, and the states work the same way. You pay as you earn, four times a year.

When are quarterly taxes due?

Here is where it gets strange. You would think each payment is due the month after the quarter ends. It is not. The real schedule looks like this:

- First quarter: April 15

- Second quarter: June 15

- Third quarter: September 15

- Fourth quarter: January 15 of the following year

Notice the second-quarter payment is due just two months after the first. Mark these dates. Missing one starts the interest clock.

And no, filing an extension will not save you here. An extension buys you more time to file, not more time to pay. The clock still runs from the original due date.

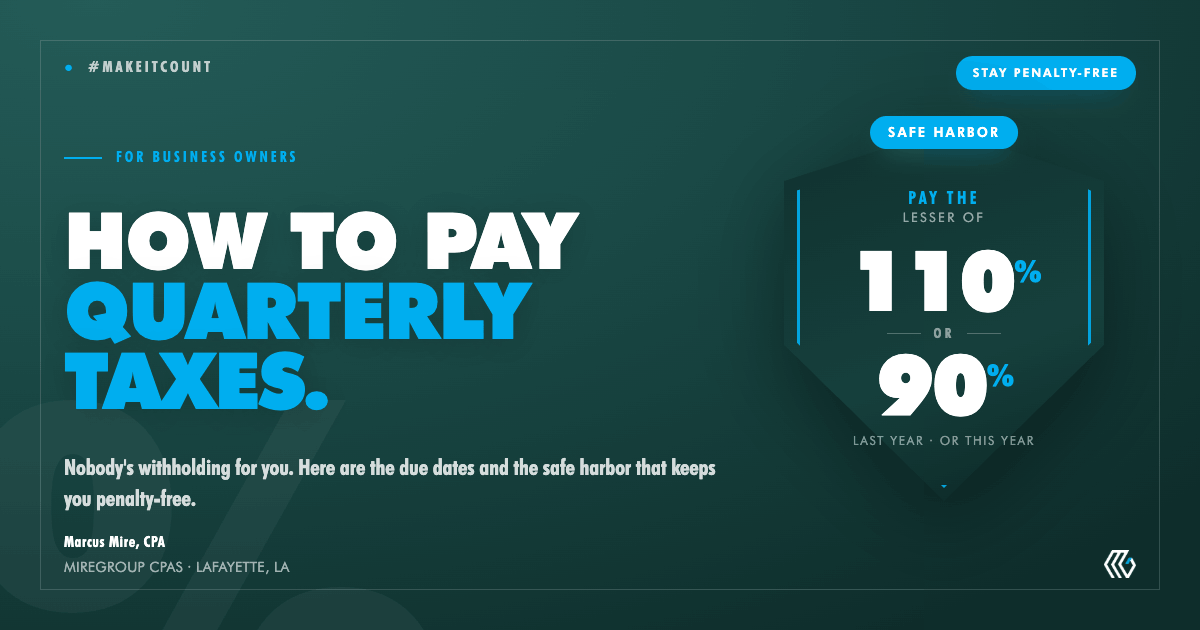

What is the safe harbor for estimated taxes?

The safe harbor is the part that protects you. It is the amount you have to pay in so the IRS does not hit you with the underpayment penalty. And that penalty is really just interest, currently running about 6% to 7% based on current IRS rates.

To stay safe, you pay in the lesser of these two amounts:

- 110% of last year's total tax, or

- 90% of this year's total tax

Here is the catch. You do not know your current-year number yet. It is a moving target all year. But last year's number is fixed. Pull your prior-year return, go to the total tax line, and you have it.

Quick example. Say your total tax last year was $100,000. 110% of that is $110,000. Divide by four and you pay in about $27,500 per quarter. Hit that and you are inside the safe harbor. No penalty.

How the safe harbor can save you money (the part most people miss)

Meeting the safe harbor keeps you penalty-free. But there are actually two calculations running at the same time, and this is where people trip up:

- The safe harbor: what you must pay quarterly to avoid the penalty.

- Your actual liability: what you truly owe when you file.

Those are not the same number. Say you are having a big year. Last year's tax was $100,000, so your safe harbor is $110,000. But you file, and your actual tax for the year comes in at $200,000.

You had two choices. You could have chased the current year and paid in around $45,000 a quarter. Or you could have paid the $27,500 safe harbor each quarter and paid the remaining $90,000 when you filed in April.

Both avoid the penalty. But the second option means you held onto that $90,000 longer. If it is sitting in a high-yield savings account, a money market, or an escrow account earning interest, it is working for you all year instead of sitting with the IRS.

That is the strategy. Pay the safe harbor. Set the difference aside somewhere it earns a return. Pay the balance when you file.

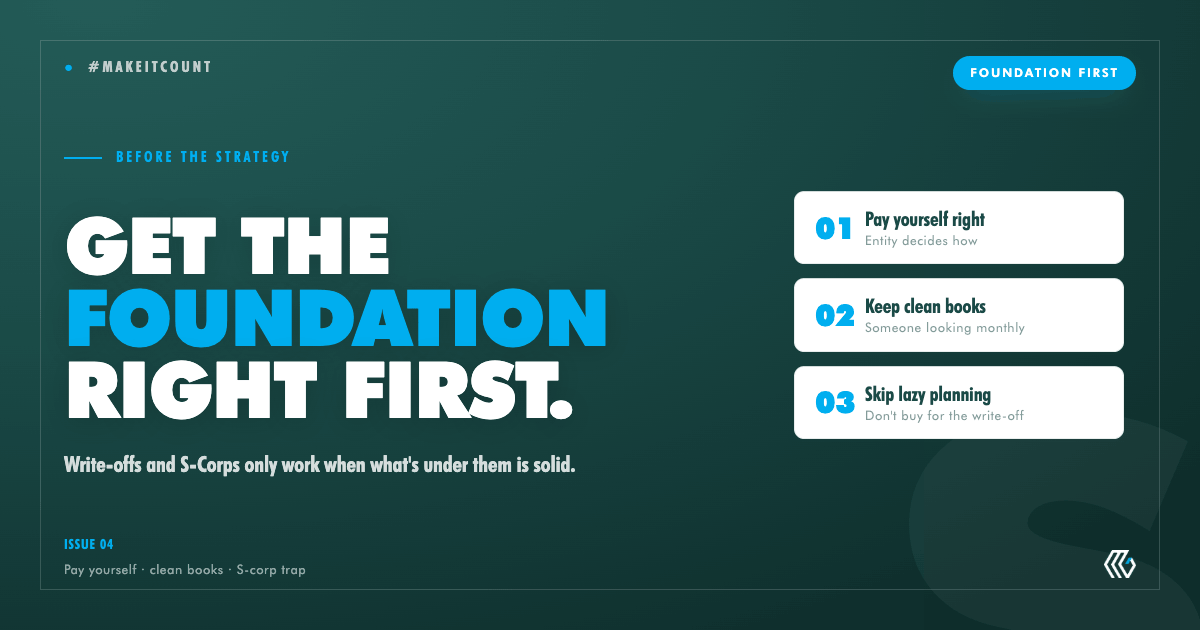

Why does this only work with good accounting data?

None of this works if you are flying blind. To pay the safe harbor and confidently set the rest aside, you need a real projection of where the year is landing. That takes current, accurate books.

This is what year-round tax advisory actually looks like. We have access to our clients' bookkeeping, or we do it ourselves. So we can project the year, tell you exactly what to pay each quarter, and tell you how much to park for April.

Without that, one of three things usually happens:

- You get surprised, owing far more than expected or getting a big refund you did not plan for.

- You pay the wrong amount and owe a penalty.

- Your money sat idle all year instead of earning for you.

What happens if you just file and forget?

A lot of business owners work with someone who files the return, hands them next year's estimates based on last year, and disappears. That is better than nothing. But if nobody is watching the current year, you are exposed to all three problems above. Those estimates were a snapshot. Your business is a moving picture.

At MireGroup we work with clients on this all year, because we have their numbers in front of us. If you want quarterly taxes to stop being a guessing game, we'd love to help. We walk through the whole thing here at mire.group.

#makeitcount

Frequently Asked Questions

Do I really have to pay taxes quarterly?

If you have income without withholding, such as business, consulting, or gig income, yes. The IRS is a pay-as-you-go system, and so are the states. You are expected to pay in as you earn, not settle up all at once in April.

What are the quarterly tax due dates?

April 15, June 15, September 15, and January 15 of the following year. They are not evenly spaced, which catches people off guard. The second-quarter due date is only two months after the first.

What is the underpayment penalty, really?

It is interest on the tax you should have paid quarterly. Right now it runs about 6% to 7% based on current IRS rates. You avoid it by meeting the safe harbor.

What is the safe harbor amount?

The lesser of 110% of last year's total tax or 90% of this year's tax. Last year's number is fixed and easy to find on your prior return, so most people plan around that.

Can I pay the minimum and invest the rest until April?

Yes, and done right it is smart. You pay the safe harbor to avoid the penalty, then set the remaining balance aside in an interest-bearing account until you file. It only works if you have a solid current-year projection, which comes from good books.